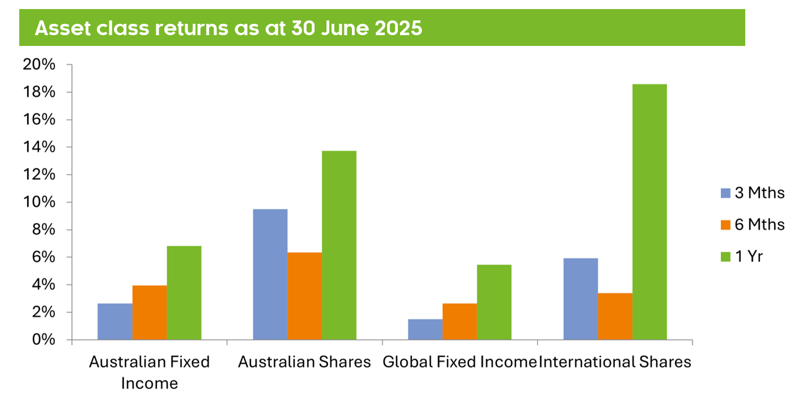

The year started with palpable enthusiasm, with equity markets rejoicing around incoming President Trump’s pro-growth and deregulatory agenda. This optimism was further fuelled by strong corporate earnings and signs of dwindling inflation, which appeared to vindicate central bankers in their multi-year battle to contain price spikes.

Mag-7 to Drag-7

However, as is generally the case in markets, this complacency was quickly uprooted in late January by the emergence of DeepSeek, a purportedly low-cost Chinese AI startup. DeepSeek threatened the dominance of the incumbent US tech giants in the AI arms-race, which caused markets to abruptly trade down.

Interestingly, markets quickly challenged the narrative coming out of China, and whilst this announcement ultimately only inflicted a flesh-wound on markets, it was the start of a bout of uncharacteristic underperformance for US markets. This underperformance would compound as the year wore on and highlights the importance of regional diversification when constructing portfolios.

The art of the deal

Through February and March, the drumbeat of tariff headlines intensified and market sentiment, mostly in the US, soured further. The aggressive and unpredictable nature of US tariff policies created a persistent cloud of uncertainty which made it difficult for businesses in the US to forecast earnings.

This was further exacerbated by tangible fears of global supply chains grinding to a halt. Investors fretted over visions of empty ports, paralysed shipping containers, and the looming possibility of empty shelves in shops.

In a notable shift, this led to meaningful outperformance for European and Emerging Markets, which settled slightly below record highs by the end of the March quarter. And whilst our domestic market remained somewhat insulated from these ructions, we weren’t immune due to the softening in commodity prices – such as iron ore – given Australia’s strong reliance on these exports.

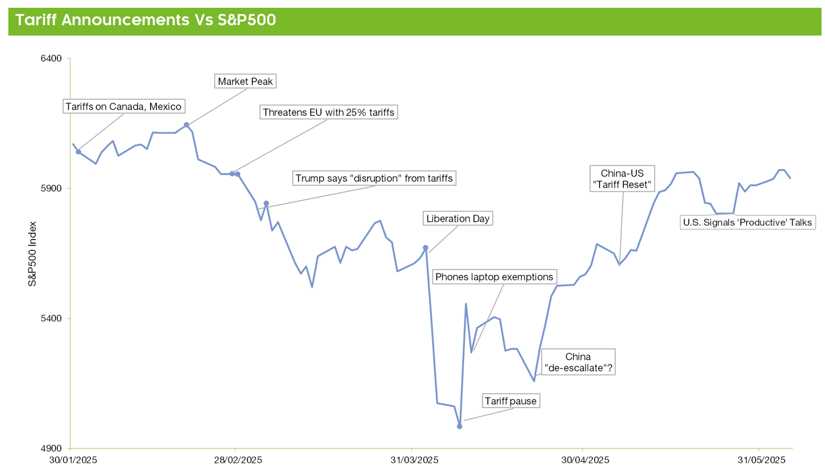

As the second quarter commenced, this uncertainty left investors with a sense of unease as ‘Liberation Day’ approached. As the below chart highlights, the velocity of information that the market was grappling with had severely fractured investor confidence and delivered a white-knuckle ride for markets.

Manic Monday

For the Australian market, this culminated in ‘manic Monday’ on 7 April 2025. The ASX200 Index plummeted in response to escalating global trade tensions, marking its worst day of trading since the COVID-19 pandemic began in March 2020.

Fortunately, the panic was short-lived as the Trump administration soon thereafter announced a 90-day pause on the most severe tariffs to allow for negotiations to take place. This rapid reversal sparked a severe relief rally which caught many investors wrong-footed, especially those who had bearishly positioned their portfolios for what they believed was the imminent breakdown of global trade.

The best days follow the worst days

Importantly, up until this point, our Portfolio Solutions team had engaged in extensive discussions as to whether we should de-risk our portfolios. Ultimately, given the elevated volatility and a lack of visibility over a potential trade war resolution, we opted to stay invested through this period.

What followed was an historic run for equities, particularly in the US where the S&P500 surged by 9.5% in a single day, marking the third best day on record for the index. And as is typically the case in bouts of extreme volatility, the best days tend to follow the worst, which highlights the importance of staying-the-course through these periods.

Sell in May & go away?

This set-up May for another strong month of returns across all equity markets, but in particular domestic and global small and mid-caps where we’ve built up modest overweight positions. The only real blip for the market through May was the downgrade of the US sovereign credit rating by Moody’s, although the market response was largely muted.

However, the downgrade did underscore growing concerns about the US’ ballooning debt burden, particularly given Trump’s signature ‘One Big Beautiful Bill Act’ which was formally introduced into the US House of Representatives over this period. This caused consternation given the bill’s embedded tax breaks and resultant increase in the US budget deficit, and potential for flow-on effects to higher bond yields.

Escalate to de-escalate

As we reached the midpoint of the year, equities remained largely buoyant, despite escalating tensions in the Middle East provoking fresh anxieties. This conflict abruptly hit its crescendo as the US launched a decapitation attack against Iran’s nuclear facilities.

And in a surprising twist, markets again appeared sanguine against this backdrop, perhaps due to Iran’s ability to strike back being severely hobbled. That said, this again served as a reminder that markets tend to look-through geopolitically instability fairly quickly.

Climbing a wall of worry

Over the course of this year, we’ve seen the pendulum swing from record highs to a bear market for US equities and back again. And as we commence a new financial year and Trump’s 90-day tariff pause has come to pass with little market reaction, it appears that investors have come to the realisation that tariffs are negotiating tools rather than absolutes.

Importantly, President Trump appears cognisant of weighing the competing priorities of generating tariff revenue to support his fiscal agenda, with the market rioting if he pushes too far. Moving forward, we remain constructive on the market outlook and are leaning into segments that offer attractive value, such as Global Listed Property, Global Small and Mid-Caps and Emerging Markets.

And as the market continues to climb its wall of worry, we’ve balanced the need for defensive anchors with the potential for growth. Our client portfolios have protective measures for the volatile moments and remain sufficiently agile to participate in the ascent.