Interest in real assets continues to attract attention as more investors take note of their defining characteristics – a smoother set of returns that are lowly correlated with other major asset classes.

However, while real assets are characterised by lower volatility, this can also create a paradox for the unwary. Reducing volatility is not the same as reducing risk. Structural aspects of real assets such as long investment timeframes, illiquidity and leverage, work to heighten complexities and risk at the individual fund level. Low volatility potentially masks the seriousness of these risks for the unsuspecting investor.

While we have advocated the attractive attributes available in real assets for years, we believe many investors do not fully appreciate the inherent restrictions that must be accepted to fully reap the benefits.

Real assets defined

A fundamental characteristic of real assets is their tangible nature, with returns typically underwritten by a consistent income stream. Real asset generally comprises the following categories:

|

Real Assets Categories |

Sub-categories |

| Real estate | Office, retail industrial, multi-family (US, Europe), residential, healthcare, self-storage, leisure |

| Infrastructure | Airports, shipping ports, rail, toll roads, social infrastructure, renewables, transport leasing (aircraft, energy logistics) |

| Natural resources & commodities | Agribusiness, energy, metals & mining, timberland & forestry, water |

Within each of these categories, there can be a wide range of market sectors, strategies and risk profiles depending on the strategy and inbuilt leverage.

The industry generally views unlisted securities (or direct ownership) as the purest form in which real assets can be held and still retain their fundamental characteristics. While we are strongly supportive of investing in listed real estate and infrastructure, the characteristics of these assets are naturally altered by introducing liquidity.

Often highly localised in terms of their trends and drivers, real assets are nevertheless underpinned by similar fundamentals, key demographics such as population growth, immigration and urbanisation. Given their localised nature and generally lower individual diversity than liquid securities, they are often subject to more idiosyncratic risk.

While there is a large range of illiquid asset classes available in a global context, most funds currently available to Australian retail and non-institutional investors comprise real estate and to a lesser extent, infrastructure. However, many of the key considerations around using real assets remain applicable.

What are the characteristics of real assets?

|

Pros |

Cons |

||

| Income generation | Resilient source of real income, cashflows often contractually agreed with set increases over time. | Illiquidity, transparency | Real assets are by nature a long-term asset class and illiquid. The more liquidity is added, the more the economic performance deviates from fundamentals drivers. Transparency of pricing is also typically lower than for liquid assets. |

| Low correlation to liquid asset classes | Historically stable, low correlation to liquid assets, even in turbulent markets. | Inbuilt leverage | Prudent capital management can be strongly additive to returns if not taken to the point that asset pricing becomes unstable and detrimental to the equity position. |

| Inflation sensitivity | Many real assets have revenue which is linked to inflation, making them an attractive source of real income. While real assets are inflation sensitive, this is typically more inflation linkage than inflation protection. | Asset concentration | Assets are highly locational, capital intensive and not easily divisible, meaning a representative market exposure cannot be built with a small number of assets. Most portfolios are relatively concentrated compared to liquid securities. |

| Long duration (asset & liability matching) | Relative to liquid assets, investor holding periods and cash flows tend to be long duration. This can make funds holding these assets attractive when matching asset and liability requirements in portfolios. | Slow capital deployment | Illiquid, large scale, assets means capital deployment can be slow, resulting in opportunity losses as capital get put to work. |

| Active management & value creation | Real assets require intensive operational input to deliver best outcomes. Unlike liquid securities, there are multiple points of returns generation from asset management which can be less dependent on market cycles. | Higher cost | Real asset funds generally have higher fees than liquid asset classes (on a net asset value basis). However, active management aspects can attenuate this impact. |

Given their diversity, the expression of various factors that drive investment outcomes can be stronger or weaker in individual funds depending on their individual strategy and the structure. The following table provides a snapshot of these high-level factors and their indicative strength.

Zenith views the following key aspects as critical to understanding real assets.

Cashflow generation

Real assets are often sources of high yielding real income. Cashflows can be highly predictable, providing a compelling option for investors with regular cash distribution requirements.

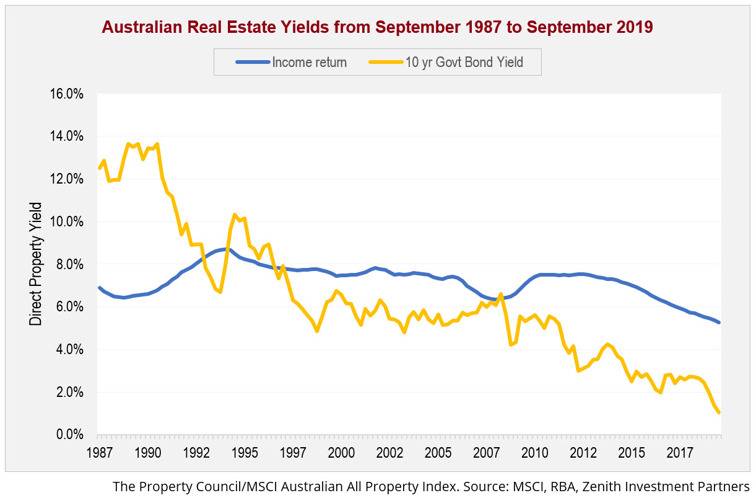

As an example, the following chart illustrates the rolling yield spread achievable in Australian commercial real estate relative to the risk-free rate. Real estate is typically a resilient source of income and unlike equities whose distributions are discretionary, income is contractually agreed and typically increasing over time with contractual uplifts.

Low volatility / low correlation

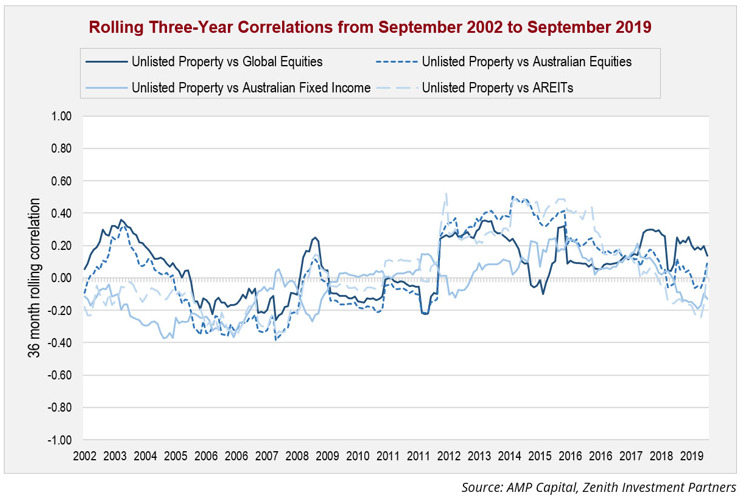

Real assets historically low correlation to liquid assets is one of the most powerful attributes of the sector for diversifying portfolio returns. A key driver of these lower correlations is illiquidity. While there is a connection between liquid and illiquid real assets given commonality in fundamental drivers, these are typically weakened by market sentiment in liquid securities which is faster moving.

The following chart shows the three-year rolling correlation of returns (net of fees), for Australian unlisted real estate funds (MSCI Core Wholesale Monthly Property Fund Index).

Individual exposures can also be highly differentiated owing to locational aspects, asset duration, fund structures and leverage. As such, correlations between real asset segments also tends to be low due to their individual drivers.

Fundamentally, such analysis tends to raise the following question: do correlation benefits reduce if data is de-lagged and/or de-smoothed?

While the answer is yes, in many ways this does not reflect the reality for investors. For portfolios, fund-level data for pricing applications, redemptions and distributions is a tangible experience. While unlisted asset prices rise and fall on a lagged basis, these tend to be offset by liquid securities being quicker to both fall and recover, reducing this effect.

Leverage

Leverage is often seen as an efficient use of capital in real assets given their cashflow generating properties and capital intensity. Prudent leverage can be an additive aspect of return generation, if not destabilising to asset pricing and the equity position. However, higher leverage skews risks and potentially limits management’s ability to navigate risk events.

Suitability of leverage should be a fund specific question. The following questions may aid in framing suitability of target leverage.

- Assets: Quality of assets and tenants? Ability to generate stable income? Diversification of security assets? Strategic plans for assets?

- Cashflows: Are weaknesses in cashflows present that may impede debt serviceability? Do they intersect with debt maturities?

- Debt facility: What are the debt covenants? Debt duration and maturity profile? Diversity of debt sources? Hedging profile?

- Does the holding structure (i.e. open or closed-ended fund) impact financing? What does this mean for capital management strategies?

Logically, utilising leverage is riskier at the top of the market than at the bottom. Ironically however, until cycles reach their peak, availability of credit is often harder to access at the bottom of the cycle rather than the top.

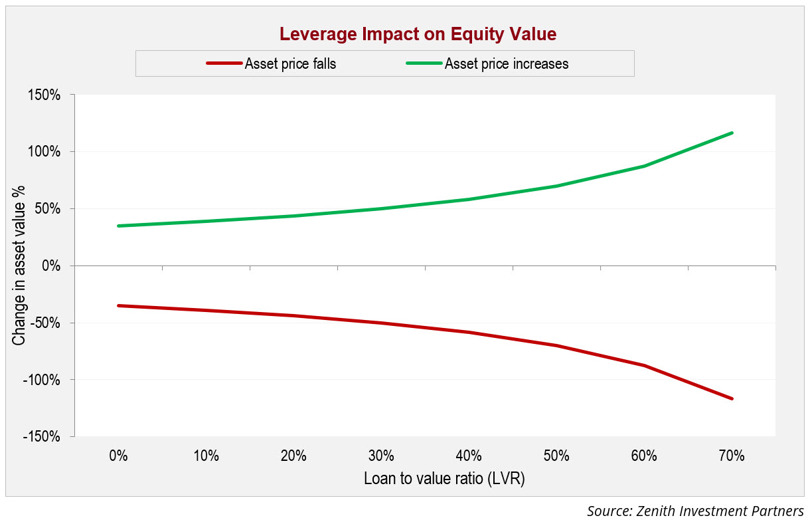

While the appropriateness of leverage must be assessed at the individual fund, and if necessary, asset level, some basic thresholds can be simulated. The following chart outlines the impact of leverage on investor equity relative to asset pricing.

While this is a best case/worst case scenario as it does not account for holding periods, it illustrates the increasing destabilisation of the equity position when taking on higher leverage. The implications of this simulation are broadly that once leverage reaches 45%, downside risks increase rapidly. This supports our long-held belief (and market observations) that leverage rates at this level or higher are generally unpalatable unless material mitigating factors are present.

Illiquidity

Illiquidity is a significant driver of real assets low correlation characteristics and is an unavoidable aspect of the asset class. The more liquidity is added, the more the economic performance of real assets deviates away from the fundamentals which drive it.

While sacrificing liquidity can be profitable, liquidity mismatch is inherent for vehicles that offer short-term redemptions while holding long dated assets. It should be considered as a necessary trade-off and form part of a robust risk assessment.

For fund managers, managing liquidity is a particularly demanding challenge. When liquidity is too low, the fund faces greater risk of suspending redemptions should it face adverse market conditions. Conversely, where liquidity is too high, this may dilute performance (cash drag) or add volatility (listed securities).

While some form of liquidity mechanism is required in an open-ended fund, investors should consider that liquidity mechanisms may only operate effectively when markets are relatively stable. Any severe enough loss of confidence and an associated call on redemptions is likely to see a fund alter or suspend redemptions. Investors should keep in mind that fund liquidity generally mirrors that of the underlying assets.

Lessons from previous real estate cycles suggest liquidity mechanisms cannot always meet redemption demand at peak periods. A realistic outcome is to expect that there are situations under which liquidity will be unobtainable.

Compensation for illiquidity also varies over time. Investors tend to demand high compensation for illiquidity during a downturn, often to the extent that liquidity becomes unavailable at any price. Conversely, compensation for illiquidity is often ignored at the peak of the market.

Diversification

Unlike most liquid assets, real assets cannot be accessed via an indexation strategy. Given the highly locational nature of assets and attendant high asset-specific risk, this also means a representative market exposure cannot be built with just one or two assets. As a result, building a large enough portfolio to truly represent an investible market is difficult.

Notwithstanding that many real asset funds pursue sector-specific strategies, by nature most are concentrated relative to large liquid counterparts (and their investible markets as a whole).

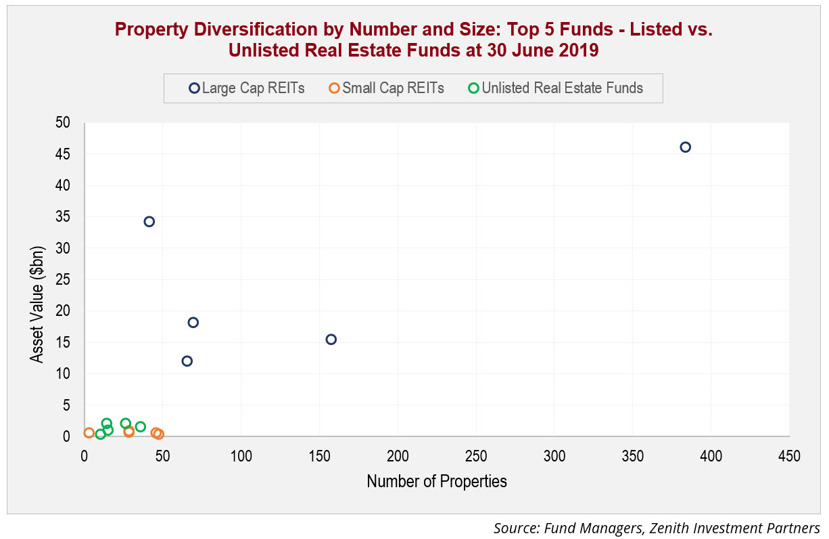

Using Australian real estate as an example, the following chart shows concentration in terms of the number and value of assets across listed and unlisted real estate funds. Included are the five largest large cap and small cap Australian Real Estate Investment Trusts (AREITs) relative to that of Zenith’s five largest rated Australian unlisted property funds (by value).

While these unlisted property funds have materially greater diversification than traditional property syndicates (typically small closed-ended funds often with a single asset), their diversification attributes have much in common with small cap REITs. Purely from an asset risk perspective, investors should consider the implications of relatively concentrated portfolios.

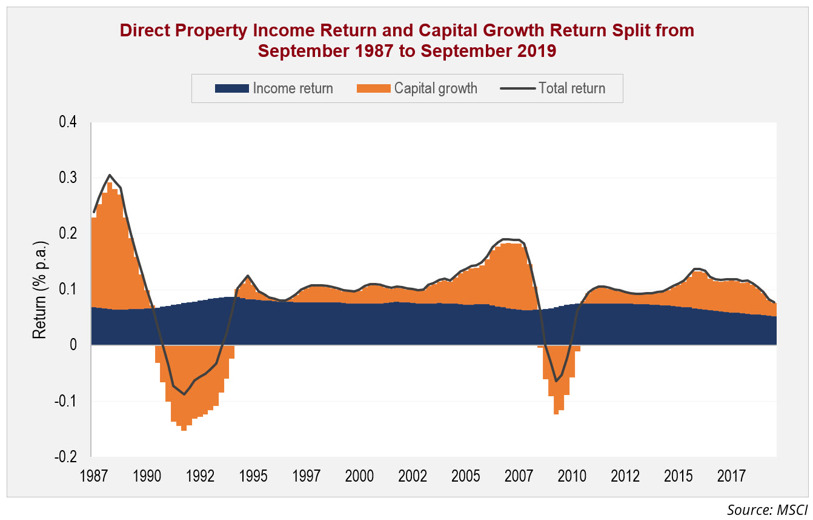

This is important when considering volatility of total returns. Over the long-term, core commercial real estate typically generates approximately 70% to 80% of its total return from income and 20% to 30% from capital growth.

However, from a volatility standpoint, the reverse is true where at least 80% of the risk typically comes from the growth component.

In the following chart, the relationship between volatility in income and growth in Australian real estate is evident.

As such, capital risk becomes elevated in smaller portfolios with greater idiosyncratic risks which are less able to be diversified away. Investors need to focus on the appropriate timeframe of a strategy, the strength and duration of lease counterparties and the potential for market-led reversions in income. Ultimately, while real estate portfolios typically have lower diversification than equities and fixed interest portfolios, this can also be reduced by active operational management.

Conclusion

We believe that overall real assets offer a compelling proposition for those seeking to access physical assets which have many attractive characteristics in a portfolio context.

However, the decision to add such assets must be highly sensitive to illiquidity risk tolerances and structural constraints. We believe that the full potential of these assets can only be realised in a strategy that is liquidity constrained. As such, it is important for investors to ensure that their portfolios are appropriately constructed to deal with a real asset allocation to ensure optimal outcomes.