Market neutral strategies are designed to target stock-specific risk/return outcomes, regardless of the market environment. Paramount to this design is a fund’s ability to hold offsetting long and short portfolios that largely eliminate market risk from return outcomes.

How effective have Zenith’s rated funds been in eliminating market risk?

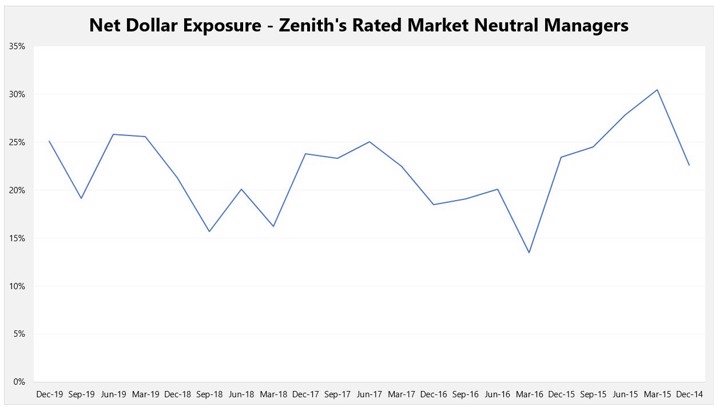

The dollar difference between a strategy’s long portfolio and short portfolio is its net dollar exposure. The chart below shows the average net dollar exposure among our rated market neutral managers.

Source: Fund Managers

Although a common expectation for market neutral funds is that their net dollar exposures should be close to zero, Zenith found that our rated funds maintained an average net long bias of 20% to 25% over the past five years.

What is net beta exposure and why is it relevant?

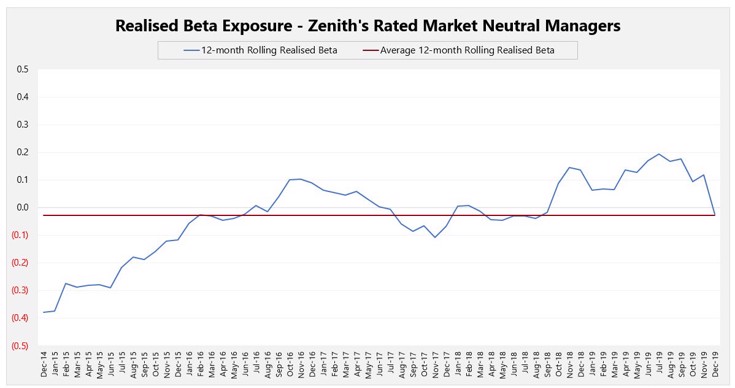

Although our rated funds have maintained a net long dollar exposure, we do not believe this measure is completely reflective of market neutrality, with beta neutrality our preferred metric.

Beta represents the sensitivity of an asset’s price return to the movements of the broader relevant index. Like net dollar exposure, the beta of market neutral strategies is the difference between the beta of the long and short portfolios.

The chart below shows the beta exposure of our rated market neutral managers.

Source: Fund Managers

Our managers exhibited an average realised beta of close to zero over the past five years, which suggests that the performance of our managers exhibited virtually no sensitivity to broader Australian equities.

How does a net long dollar exposure result in a net beta neutral outcome?

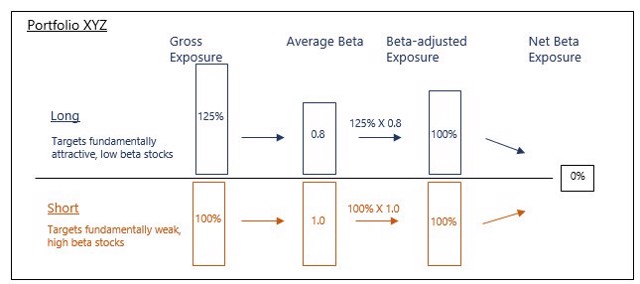

The outcomes produced by market neutral funds can be explained through the different dynamics that typically drive the long and short portfolios, explained by the diagram below.

Source: Zenith Investment Partners

We believe this dynamic is representative of most of the market neutral funds we cover. We have identified the following key reasons for this relationship.

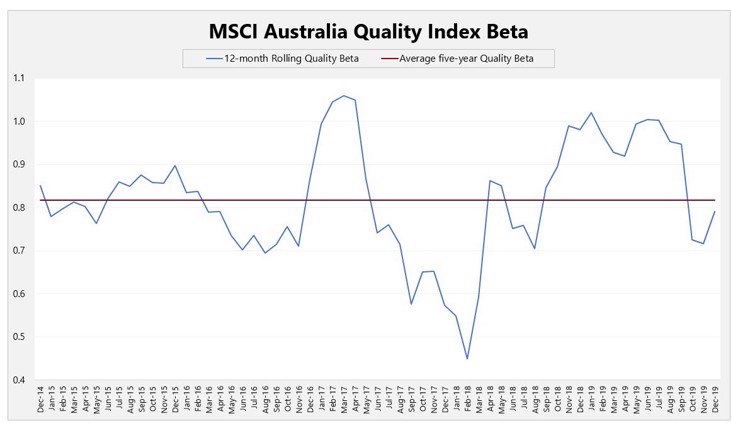

Managers typically hold “quality” stocks long

Managers tend to buy high quality businesses and short-sell troubled businesses.

The chart below shows the beta of Australian quality companies, as represented by the MSCI Australia Quality Index.

Source: Bloomberg, Zenith

The chart highlights that higher quality companies are generally less sensitive to movements in the Australian equity market, given the average beta of less than 1.

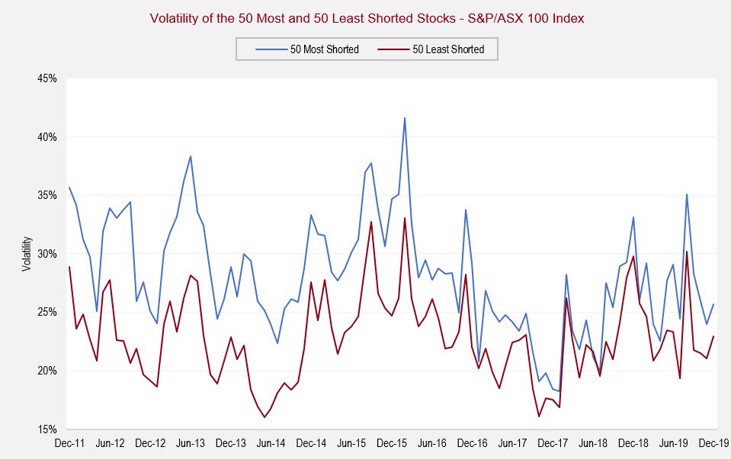

Shorted stocks are more volatile

Troubled businesses pressured by short sellers tend to exhibit greater levels of volatility, as shown by the chart below.

Source: Bloomberg, Zenith

We believe this positive relationship between short interest and volatility is consistent across broader Australian equities. In addition, we found that the average beta amongst the 50 most shorted stocks was 1.01 compared to 0.91 for the 50 least shorted stocks.

There is more to market neutral strategies than just stock picking!

Whilst market neutral strategies tend to be viewed as pure stock-picking exposures, we believe the concepts of dollar and beta neutrality are critical factors in ensuring attractive returns that are independent of market direction.