Tensions between the US and Iran reached a fever pitch on 28 February, as hostilities escalated into US-Israeli strikes. The military campaign - ‘Operation Epic Fury’ - targeted Iranian leadership, military sites and nuclear-related infrastructure.

Iran subsequently responded in kind, initially targeting US bases in Bahrain, Qatar, Kuwait, and the UAE, as well as more indiscriminate attacks against Israel. However, these attacks have broadened into strikes against oil and gas production facilities, luxury hotels frequented by Westerners, embassies, airports and shipping – which was an escalation largely unexpected by markets.

Of course, our thoughts are first and foremost on the human toll exacted by war, yet from a market perspective, we outline below the implications for client portfolios.

Sell first, ask questions later

Source: Zenith Investment Partners

The initial market reflex reflected a more traditional geopolitical risk-off posture, with safe haven currencies (USD, Swiss Franc, Japanese Yen) and gold rallying. Optimism initially centred on this being a ‘one and done’ shock, whereas now markets are grappling with the potential for a period of prolonged volatility.

A week later, the window of uncertainty has broadened, raising the probability of wider tail risks, elevated energy prices and heightened risk aversion. This, in turn, forces a reassessment of market risk premiums to reflect a less forgiving growth and inflation backdrop.

Crude oil on the boil

The first-order transmission mechanism to the real economy has been through higher oil prices, with Brent crude briefly peaking at US$119 per barrel, before softening to around US$88 per barrel at the time of writing. Crucially, this remains a material increase from US$72 the day prior to the strikes and around US$60 at the start of the year. The catalyst has been the effective closure of the Strait of Hormuz and disruptions to Qatar’s liquefied natural gas industry, placing roughly 20 per cent of global oil and LNG supply at risk. We are already seeing the ripple effects in higher prices for refined products such as diesel, jet fuel, shipping fuel, gasoline and petrol.

Given our increasingly interconnected global economy, this will have flow-on effects to higher inflation and bond yields. For our client portfolios, we remain comfortable with our underweight duration positioning, yet are conscious of the risk of a spike in bond yields and would look to take advantage of any sustained move higher by increasing our government bond exposures.

Drill baby drill

Given a centrepiece of Trump’s campaign emphasised lower energy prices, it’s difficult to reconcile how a protracted quagmire in the Middle East would support these aims. And with the midterm elections on the horizon, the Republicans can’t afford the optics of another endless war and a sustained increase in petrol prices.

There’s also immense pressure from the Gulf states to find an off-ramp given the monumentally negative impact this is having on their efforts to diversify away from a reliance on oil exports into tourism. For these reasons, logic would dictate a diplomatic solution is best for all involved, yet logic doesn’t always dictate outcomes in these scenarios.

Investing at high altitude

Although Australia is geographically removed from the direct conflict risks, there‘s no escaping the impact at the bowser. It’s estimated that each US$10 increase in oil prices translates to roughly a 10 cent per litre rise in petrol prices. Australia is also exposed through a global supply chain that relies heavily on the transportation of goods across the globe.

These points, coupled with the fact that Australia has only approximately 34 days of refined fuel reserves, make walking the inflation tightrope even more delicate for the RBA. A supply shock stemming from the conflict in the Middle East could arrive at precisely the wrong time, when inflation is uncomfortably high and the RBA has been abruptly jolted back into a hiking cycle. Consequently, we are closely monitoring any shifts in market inflation expectations and rate hike pricing, and the potential implications for credit markets and small-cap equities within our portfolios.

Gold bugs

The curious reaction from gold similarly warrants discussion. In the initial aftermath, gold rapidly pumped higher, only to consolidate modestly lower in the days thereafter. This can primarily be attributed to two key drivers: profit-taking, given gold’s meaningful rally, and a rising USD and bond yields making a non-income producing asset relatively less attractive.

In this environment, it’s easy for noise to swamp signal and for nuance to be lost. Longer term, we continue to view gold as an attractive inflation hedge in an environment of monetary debasement and central bank buying.

To ensure adequate look-through gold exposure for our clients, we express this view through either a dedicated gold allocation or through ensuring a complementary blend of active managers with sufficient underlying exposure to gold miners.

Fog of war

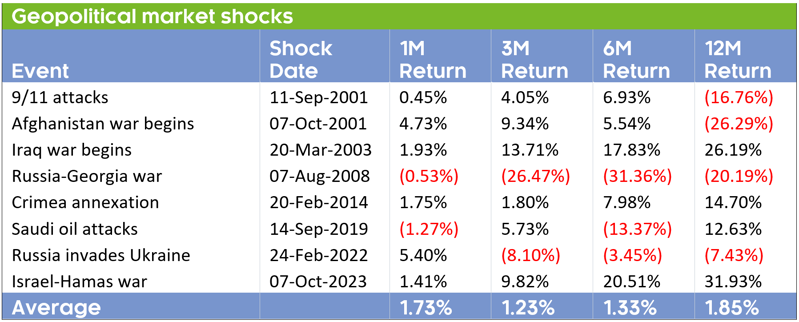

Given markets’ nervous response to these geopolitical tussles, we’re hearing reports from advisers that they’re fielding calls from clients querying whether they should be redeeming into cash. Whilst it’s impossible to accurately predict market moves amidst the fog of war, we have numerous precedents in which markets digest the volatility and refocus elsewhere.

Source: Zenith Investment Partners

Although the above table does show periods of negative returns, there’s no clear pattern of market behaviour following geopolitical shocks. And, generally speaking, the market tends to fairly quickly look through the fog of war and climb the wall of worry.

Black gold

Importantly, should markets conclude that the war objectives have narrowed, retaliation is more contained and oil flows re-open, then the impact on portfolios shouldn’t be too destabilising. With oil flows representing one of the key chokepoints for markets, we ‘re encouraged by the US announcement that it will provide naval escorts through the Strait of Hormuz, alongside insurance guarantees for tankers transiting the Strait.

As at the time of writing, this has yet to produce any meaningful reduction in the war-risk premium embedded in oil prices, but it does indicate the seriousness with which the US administration is seeking to prevent further oil price spikes.

Playing with a loaded gun

The regional fallout has been swift, with the conflict already touching a dozen or so countries. However, at this juncture, we don’t foresee a correction morphing into a painful bear market. This is principally due to constructive macro conditions, supportive fiscal settings, improving corporate fundamentals, resilient labour markets and mostly accommodative monetary policy (outside of Australia).

What does warrant a cautious outlook is the richness of valuations across many markets. For this reason, we emphasise regional diversification away from the US tech sector (particularly into emerging markets), in addition to market cap diversification both domestically and abroad where valuations and earnings growth are more appealing.

This is evidenced beneath the surface where there has been a significant rotation out of the mega-cap stocks, with market leadership favouring mid and small caps. We view this broadening market as positive, as portfolios are no longer reliant on tech stocks for the heavy lifting.

Notably, for client portfolios running an ‘Alternatives’ program, we expect positive attribution from the non-traditional return streams accessed through managed futures and gold. Pleasingly, we’re already seeing these allocations assist in buffering the broader portfolio volatility through their uncorrelated exposures. Similarly, for portfolios anchored to mainstream asset classes, we’re seeing the ‘Value’ exposures deliver outperformance, highlighting the benefits of style diversification.

Good buy or goodbye?

This broadening out of market leadership is generally positive, as investors are no longer so reliant on a narrow group of tech stocks to drive returns. However, the market backdrop warrants intense monitoring, with our Asset Allocation Team focused on:

- the scale and persistence of Iranian retaliation

- whether the conflict remains contained within the Gulf region or broadens further, and

- direct attacks on Gulf energy infrastructure or sustained disruption to shipping routes.

Should any of these risks materialise in a meaningful way, we would reassess the macro outlook and determine whether portfolio re-positioning is warranted.

Order within chaos

For the bull case, investors appear to have become used to the Trump military playbook – big bangs and a quick resolution. The best outcome is for that to play out again, with Operation Epic Fury concluding quickly enough for investors to move on, allowing Trump to declare victory without provoking the fury of markets.