For decades, private markets were largely the preserve of institutions - sovereign wealth funds, super funds and ultra-high-net-worth investors with patient capital and specialist access. That’s now changing.

Improved fund structures, greater platform capability, and growing adviser sophistication have steadily lowered the barriers to entry. What was once operationally complex or structurally inaccessible in private markets, is increasingly being delivered in investable formats suitable for diversified portfolios.

A different engine under the bonnet

The appeal of private markets is not a novelty – it’s simply the diversification of return drivers. Private equity, private credit and unlisted real assets derive returns from sources that differ structurally from listed markets. These include operational improvement initiatives, negotiated lending terms, long-dated contractual cashflows and access to opportunities that never reach public exchanges.

Incorporating these exposures into portfolios can:

- reduce reliance on listed market beta

- introduce alternative sources of return

- enhance long-term return potential through complexity and illiquidity premia, and

- smooth portfolio outcomes across market cycles.

In an environment increasingly influenced by passive flows and short-term sentiment shifts, the ability to access differentiated return drivers is very appealing.

Reacting in real time vs over time

One of the clearest distinctions between public and private markets is how they respond to new information. Listed equities reprice instantly. Economic surprises, central bank decisions and geopolitical developments are all reflected in market prices within minutes (or seconds, depending on the liquidity of the market). The result is transparency, but also volatility.

Private markets operate differently. Valuations tend to adjust progressively as information is incorporated over time. This does not eliminate risk, but it does alter how that risk appears in a portfolio context. What looks like lower volatility is often a function of valuation frequency and the underlying asset characteristics, rather than immunity to economic forces.

Source: Zenith Investment Partners

The contrast is visible. Public market indices experience sharp drawdowns and rapid recoveries, reflecting immediate repricing. Private market exposures tend to show smoother progression – reacting yet doing so over time rather than in real time.

Ultimately, when comparing the two markets, each would have delivered similar returns over the observed period; however, the pathway was meaningfully different. For portfolio construction, this distinction matters. It influences how risk is experienced by investors and how different portfolio sleeves interact during periods of stress.

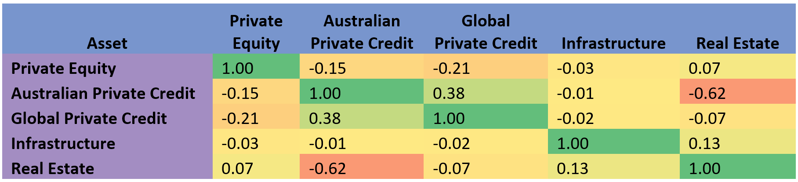

When diversification actually diversifies

Diversification works best when return drivers genuinely differ. It’s not enough to simply hold more assets - they must behave differently. Within private markets themselves, equity, credit and real asset strategies are influenced by varying cashflow dynamics, capital structures and sector exposures. The result is often low - and sometimes negative - correlation across strategies.

Source: Zenith Investment Partners

As illustrated above, private equity, private credit, infrastructure and real estate exposures do not move in lockstep. Some relationships are modestly positive, others are near zero and in certain instances, negative.

This reinforces an important point: diversification can exist not only between public and private markets, but within private markets themselves.

Liquidity isn’t free

The benefits of private markets don’t come without trade-offs – specifically, liquidity. Unlike daily-liquid portfolios, private market strategies typically offer periodic redemption windows, structured to align investor liquidity with the underlying assets. Illiquid assets require patient capital, and portfolios are more resilient when redemption terms reflect that reality.

For investors, allocations to private markets are best viewed as complementary exposures designed to sit alongside daily-liquid portfolios, not replace them.

Private markets are here to stay

As structures mature and access broadens, the conversation is shifting from whether to include private markets in portfolios, to how they should be incorporated thoughtfully within diversified portfolios.

Importantly, public speed always has its place, and private patience has its merits. The real opportunity lies in structuring both options within portfolios deliberately, integrating differentiated return drivers while maintaining discipline, governance and portfolio balance.

We’ve been working on an exciting initiative designed to do exactly that and look forward to sharing more with you in the months ahead.