The liquid alternatives sector is enjoying a renaissance, as investors focus on strategies that can perform in a range of market conditions, helping to navigate uncertainty around the Middle East conflict and growing inflationary and monetary policy pressures.

The sector is also indirectly benefiting from the growth in private assets, as advisers try to manage potential liquidity imbalances across portfolios. With the increased usage of illiquid asset classes, such as private equity (PE) and infrastructure, the importance of allocating to liquid strategies that serve a dual purpose of generating attractive risk-adjusted returns, and supporting rebalancing and liquidity management, has never been greater.

What are liquid alternatives?

Liquid alternatives are a diverse mix of investment strategies that seek to diversify traditional asset classes, such as equities and fixed income, targeting positive absolute returns from non-traditional sources of market risk premia, ie. the additional return investors expect to earn from holding a higher risk portfolio instead of risk-free assets. The range of strategies includes managed futures, global macro/absolute return, multi-strategy, tail protection, market neutral and alternative risk premia.

These strategies typically exhibit low correlation with traditional asset classes, albeit they have some exposure to macro risk factors. Let’s take a look at the main liquid alternatives styles.

Managed futures: Managers in this category use trend-following or momentum-based strategies to generate returns. This is based on the belief that markets exhibit serial correlation or trending properties (i.e. price movements in the past inform future price changes). Managed futures managers typically take long and short positions in assets which demonstrate sustained price momentum.

One of the attractive attributes of managed futures strategies is the tendency to deliver strong outperformance during stressed equity periods. For this reason, the style generally provides important diversification for traditional diversified portfolios.

Global macro/absolute return: Global macro managers employ an active approach to managing portfolios, with positioning determined through a continuous assessment of markets. This process is underpinned by macroeconomic and fundamental analysis, which is integral to the identification of mispriced opportunities.

Multi-strategy: This investment style is where managers invest in portfolios of internally or externally managed hedge fund or absolute return strategies, including long/short, equity market neutral, global macro, managed futures, currency, event driven, specialist credit, distressed securities and convertible bond arbitrage. In general, the combination of strategies is expected to offer investors a consistent return profile with a low level of volatility.

Market neutral: A market neutral strategy includes those managers that seek to identify mispricings between regions, markets and securities. The strategy is premised on building equity portfolios that display market neutrality, where long and short positions are directly linked.

Market neutral managers can utilise fundamentally driven and/or quantitatively driven investment processes with a variety of trading approaches, including pairs trading and options strategies.

Why liquid alternatives?

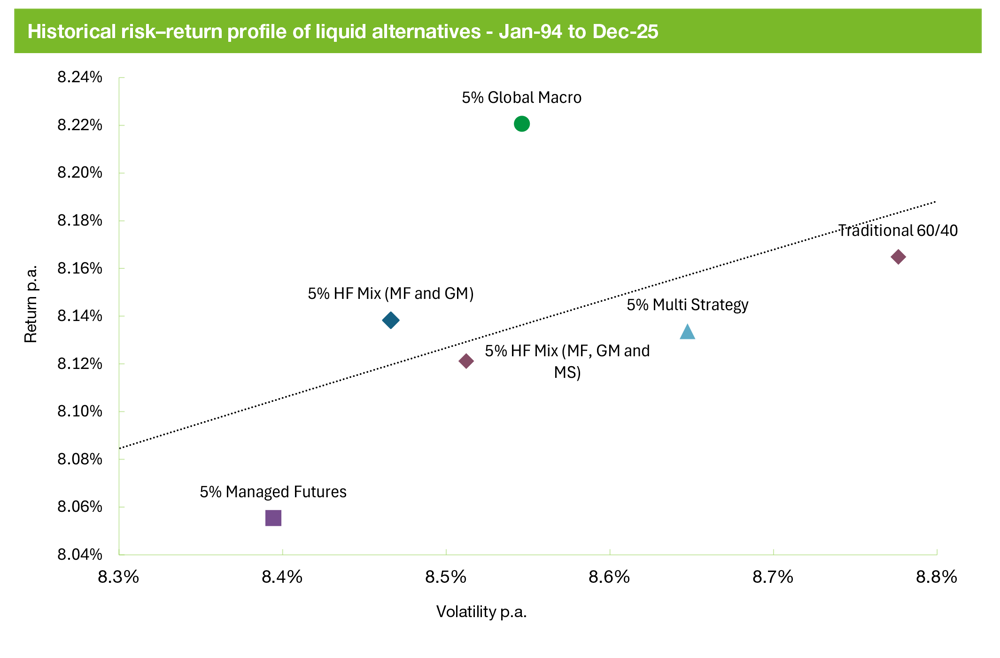

The role of liquid alternatives in a multi-asset portfolio is to provide a competitive source of returns regardless of market directionality, and importantly, diversity during risk-off periods. This is achieved through the breadth of trading approaches and flexibility to implement long and short positions. To illustrate the portfolio benefits, we assessed the risk/return benefits of adding different liquid alternatives styles to a traditional 60/40 portfolio.

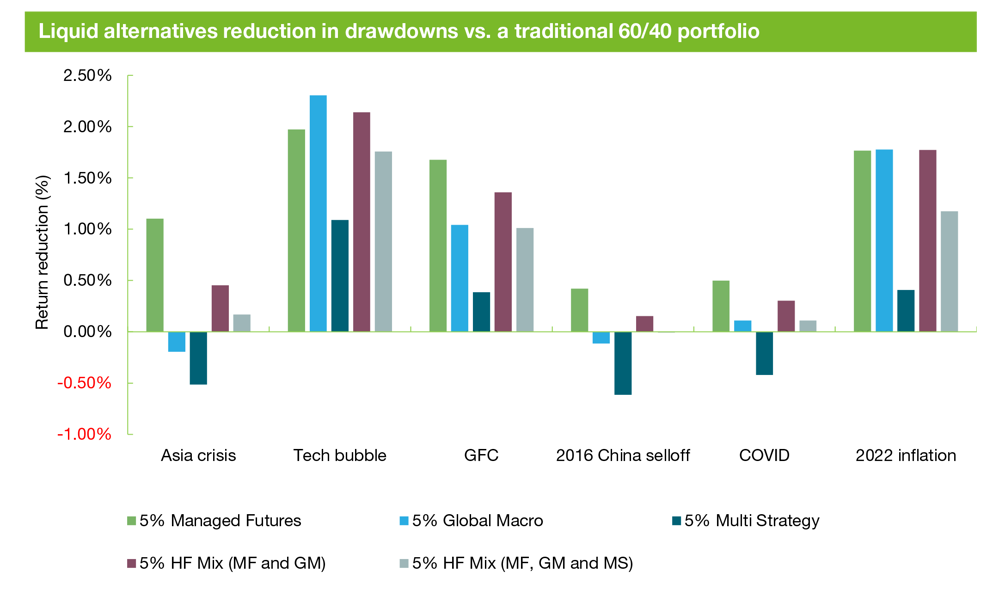

The following chart plots the risk/return enhancement from introducing a 5% allocation to different liquid alternative styles for the period 1994 to 2025. We’ve also charted the improvements in the drawdown sensitivity of each portfolio.

Source: Zenith Investment Partners, Credit Suisse Hedge Fund Indices

Source: Zenith Investment Partners, Credit Suisse Hedge Fund Indices

Across each of the liquid alternatives styles, we see reduced volatility coupled with the ability to lower the historical drawdown profile of a 60/40 portfolio. For example, through the 2022 inflation spike period, a 5% allocation to managed futures reduced the portfolio drawdown by 2% in absolute terms.

Liquid alternative managers are not expected to keep pace with strongly rising equity markets, however, they have the potential to deliver consistent returns above cash and bonds, providing important diversification.

These strategies reduce the reliance on traditional risk factors, such as equity and fixed income beta, to generate returns and introduce uncorrelated risk sources, eg. valuation mispricings between countries and sectors.

While liquid alternatives strategies are not immune to drawdowns, underperformance is generally linked to manager-specific style and strategy risk, as opposed to long-term, structural exposures to reliance on equity and bond markets.

What are the portfolio considerations when incorporating liquid alternatives?

The diversification benefits vary widely by liquid alternatives sector. In recent years, the multi-strategy style, which blends a range of strategies and alpha sources to mitigate risk, has generally been the strongest performing sector within the broader liquid alternatives universe.

Given this often leads to a more consistent expected return path over time, multi-strategy funds have, however, tended to exhibit a higher, more positive level of correlation to equity markets over time.

Regardless, the multi-strategy style performed soundly when stock/bond correlations spiked in 2022, albeit with a high level of manager return dispersion during this period.

In comparison, while managed futures have had the weakest performance across the alternatives universe over the last three years, they’ve exhibited strong diversification over time. Notably, of all the liquid alternatives strategies available, managed futures provided the strongest negative equity correlation during the weaker equity market period of 2022.

While recent absolute returns for managed futures have been lower, the ability of managed futures managers to capitalise on market shifts can depend on the efficacy of quantitative models used to identify short-term versus long-term market signals. We’ve mentioned this previously but in recent years, managers targeting faster-moving market trends have been whipsawed by sharp market shifts, and targeting slow-moving signals has generally been more effective.

Global macro is another sector with subdued recent performance in prior years, partly due to market volatility being relatively contained. However, as global macro can instead rely more heavily on manager qualitative insights, these strategies were able to better capitalise on the opportunities arising from the Liberation Day-related market volatility.

Investor awareness is key

Investors should remain mindful that outcomes can still vary by underlying investment strategy, increasing the importance of manager selection. More sophisticated investors with scale can take advantage of the benefits of low return correlation, by allocating to a broader range of liquid alternatives strategies to enhance risk-adjusted returns.