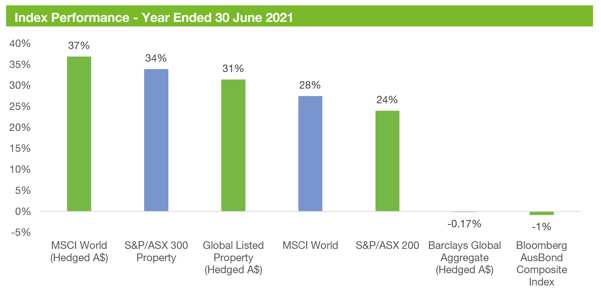

The 2021 financial year will be remembered for the phenomenal reversal that equity markets enjoyed following the economic slump experienced at the start of the year. The contrast was stark, with lockdowns and uncertainty replaced with reopening and vaccine optimism. The ensuing economic upswing saw share markets continue to march upwards, finishing the year hovering at record highs.

Source: Zenith

Fortress Australia

Initially, market leadership was narrowly confined to the secular growth stocks as ultra-accommodative monetary policy and government stimulus buoyed returns. This sentiment strongly favoured our Australian shares sleeve where we deliberately tilt our portfolio towards mid, small, and micro-cap managers which delivered exceptional outperformance for our clients.

The vaccine announcement in the latter half of 2020 spurred a historic rotation into value-oriented names which are more economically sensitive (i.e. energy and financials) and had been disproportionately impacted by the lockdowns. Pleasingly, our portfolios enjoyed leveraged exposure to the re-opening trade through our dedicated, global value manager.

Ringing the bell

Following this we modestly reduced our exposure to global long/short, which pleasingly coincided with the excess returns waning from this pro-cyclical trade. Due to the richness of valuations and crowded positioning observed in the large cap space, we opted to initiate a position in a global mid-small cap manager. Importantly, this allocation has since been vindicated with strong returns delivered to date.

The new year ushered in the Biden presidency with the Democrats wrestling control of both houses of Congress, thereby bolstering the prospects of a highly stimulatory legislative agenda. Notwithstanding the subsequent relief-rally in markets, we remained vigilant as global COVID-19 cases remained highly volatile amongst minimal vaccine penetration. Consequently, an allocation to multi-strategy was introduced into our alternatives sleeve to meet the competing pressures of delivering absolute returns through a range of market conditions, whilst exhibiting a low correlation to traditional assets.

Meme stocks burning

Market volatility broke out soon thereafter, albeit driving the market turbulence was Reddit users coordinating a ‘short-squeeze’ attack against the institutional hedge funds. This resulted in material losses for several high-profile hedge funds, as the well-publicised shorts, particularly Gamestop, shot to dizzying highs.

However, as expected, our portfolios were insulated from these gyrations, as we insist that our managers with shorting capabilities implement stringent risk control measures to circumvent any ‘short-squeezes’. In fact, our global long/short manager profited from their short positions over this period despite the broader market ructions at play.

Inflation genie

In Australia and abroad, inflation anxieties started to permeate the narrative as aggressive fiscal and monetary stimulus intersected with plunging unemployment rates. These inflationary jitters sent shockwaves through markets and left investors questioning whether central bankers might prematurely raise interest rates to choke off demand.

Fortunately, our portfolios are intentionally underweight interest rate duration in recognition of the asymmetric risk of rising rates, which could be caused by an inflation shock. As such, our portfolios have been less sensitive to broader interest rate fluctuations, and importantly, our investors experienced a more subdued pullback from their fixed income allocations over this period.

As bond yields spiked, we reduced our cash allocation and introduced a dedicated short-term credit manager. Likewise, our capital markets forecasts exposed undervalued segments in emerging markets, prompting an allocation to an ‘unconstrained’ fixed income manager with a flexible mandate targeting emerging market regions.

Mindful of the material asset price appreciation experienced in the Australian listed property market since the depths of the initial COVID-19 drawdown, we reoriented our portfolios in favour of GREITs over AREITs. Underpinning this decision was the lower volatility profile of GREITs and greater stock, sector and regional opportunities available in global listed property markets. And whilst we retain conviction in AREITs due to the yield advantages and diversification benefits, we sought more diversified exposure abroad. This concentration in our domestic market to the retail sector was soon highlighted, as the COVID-19 Delta variant prompted a new wave of national lockdowns.

Source: Bloomberg

Yield round-robin

In response, bond yields once again tumbled lower (bond yields and prices move inversely) over concerns we may have hit peak GDP growth and the ‘transitory inflation’ narrative took hold. In hindsight, our decision to exploit the dislocations in investment grade fixed income markets appeared prescient, as investors quickly flocked to the safety of these high-quality bonds. We firmly believe these decisions have optimised our portfolios for the competing pressures of liquidity, capital preservation and yield enhancement in a low-rate environment.

As the financial year drew to a close and the reflation trade lost momentum, market sentiment soon shifted back to the stay-at-home stocks (i.e. technology). We expect market leadership to continue oscillating between value and growth as the market digests the transient inflation hypothesis and the durability of the economic recovery.

We remain content with this tug-of-war, as our portfolios are appropriately diversified and not constructed based on short-term style bets. Moreover, we’re comfortable not fully participating in frothy markets, and reiterate that central to our portfolio construction is risk-management and attractive absolute-returns for our investors.

Wonder down under

As the financial year concluded and the ASX200 generated a record-setting 24% surge, optimism flourished as Australia reported GDP and unemployment back at pre-pandemic levels. However, despite vaccine penetration increasing significantly, the Delta variant bears close watching as global COVID-19 cases remain volatile. The potential also remains for inflation to overshoot, despite the emphatic guidance from global central banks that price pressures will be ‘transitory’.

Crucially, our long-term views on markets remain constructive, although we continue to advocate for high-quality, active managers to navigate this uncertain terrain over the medium-term. Moving forward, we believe that our portfolios are positioned to withstand any unforeseen shocks where market excesses are exposed, whilst remaining poised to participate in future market gains.