Key points:

|

A fundamental characteristic of real assets is their tangible nature, with returns typically underwritten by a consistent income stream. Real assets (particularly real estate and infrastructure) can be highly attractive, given their tendency to produce a smoother set of returns with low correlation to other asset classes. They also have a range of other positive characteristics, such as consistency of income at a premium to cash rates, inflation linkages and the value that can be extracted from operational management.

Private market real assets such as unlisted property and infrastructure have traditionally demonstrated low levels of correlation to public market assets. However, there are material caveats. Illiquidity is the key driver of real assets’ low correlation characteristics and is an unavoidable aspect of this long-term asset class.

Although less correlated to general equities under most market conditions, current events have highlighted that due to declining patronage levels, elements within both real estate and infrastructure are materially exposed to the fallout from COVID-19, namely retail property and transport-related infrastructure.

The liquidity conundrum

Increases in demands on fund liquidity can occur for a variety of reasons. Given the confluence of declining sentiment, market turmoil, and increasing questions around valuations, many funds are seeing an elevated level of redemption requests. For funds with less liquid assets, there is a constant struggle to manage the trade-off between liquidity, volatility, risk, and ultimately, performance.

For such funds, it is important to understand the mechanics of fund liquidity. The following elements shape a funds liquidity framework:

- Volumes and timing of applications and redemptions from investors

- Cashflows from rental income received

- Short-term cash requirements for essential expenses

- Available lines of credit

- Pricing and liquidity of assets

The threat of a liquidity mismatch is inherent for funds offering short-term liquidity while investing in long-dated assets. While sacrificing liquidity can be profitable (and enhance the risk-return characteristics of a portfolio), liquidity mechanisms cannot always meet redemption demands at peak periods. Indeed, this should be expected in times when investor confidence drops and indiscriminate selling of risk assets ensues.

Given investor confidence is being severely undermined across all markets, it is logical that real assets funds will once again find liquidity mechanisms tested and may be forced to alter redemption mechanisms. This is unavoidable.

In times of crisis, revisiting the implications and likely outcomes of a liquidity freeze is a valuable tool in managing portfolios.

Be realistic about liquidity

Investors must understand from the outset that liquidity mechanisms are at their most effective when markets are relatively stable. While the likelihood of a halt to existing redemption programs ultimately depends on the liquidity framework, any severe enough loss of confidence and associated surge in redemptions are likely to see a fund alter or suspend redemption programs. A realistic outcome is to expect that there are many situations under which liquidity will be expensive, if not unobtainable.

Understand liquidity mechanisms

Liquidity mechanisms vary widely. There are typically three major aspects:

- The amount of liquid securities held as a proportion of Net Asset Value (NAV)

- The frequency of redemption offers

- Any limits on the level of withdrawals which can be made at any one time

For many open-ended funds, a typical structure is often as follows:

- Maximum 10% liquid securities/cash

- Redemption offer scheduled every six months

- Maximum withdrawal limit per redemption offer (in aggregate) of 5% of the fund NAV

There are a wide range of combinations which can be used. For example, liquid securities can be as high as 30% or as low as zero. Redemption requests can be as often as daily or infrequently as annually. Every fund is different.

Even within such frameworks, there is considerable leeway in how long a manager can take to pay redemption requests. Under certain circumstances (such as the inability to realise sufficient assets if liquid reserves are depleted), payment periods may be extended materially, often up to 12 months. Investors must familiarise themselves with all the conditions of liquidity and consider them critically.

Understand the implications of illiquidity and plan accordingly

For investors, illiquidity risks go beyond access to capital. They should also consider:

Portfolio asset allocation: As liquid securities decline in value, exposure to illiquid assets which reprice less frequently increases. Illiquidity means rebalancing portfolios can be cumbersome and reduces the ability to recycle capital into potentially more attractive opportunities.

Ability to make tactical decisions: While long-term horizons should be embraced, material changes to a fund’s objective, positioning or management capabilities are always possible. In illiquid funds, the ability to effectively respond to sudden changes and down-weight or exit positions can be materially reduced.

Distribution cuts: Funds that alter redemption arrangements usually only do so during market turmoil. As such, income stress and lower valuations can result in the Fund’s income distributions being cut in order to fund essential asset expenditure. Investors need to consider overall portfolio cash generation carefully in stressed markets and plan accordingly.

Liquidity solutions are neither quick nor easy: For funds where liquidity is halted for prolonged periods, there are only two alternative paths to riding it out. One is a windup. This takes time as a fund must either sell assets when the market is unfavourable or wait for a recovery. The second is an ASX listing. This is frequently problematic as appetite for listings is unlikely to be attractive until volatility decreases. Also, most unlisted property funds are too small to make an attractive Real Estate Investment Trusts (REIT), meaning on-market liquidity will be shallow and price discounts to net assets is also a real possibility.

What to do?

The collapse in REITs and Global Listed Infrastructure (GLI) prices are typically a leading indicator for private market valuations in these assets. Already, institutional managers of unlisted funds are beginning to mark down asset values. Depending on jurisdictional rules regarding liquidity, some funds are already putting a hold on redemptions (UK real estate funds being a case in point). Like it or not, pricing and liquidity challenges are coming to real asset funds everywhere.

How should investors in open-ended funds be responding?

Assuming appropriate choices have been made regarding fund selection, asset allocation and investment horizons, the most realistic strategy is to ignore the threat of lower liquidity in the medium-term. This is one of the key reasons investors need to have at least a 7-year time horizon. It is also why it’s critical to partner with well resourced, established managers whose core expertise is owning and operating funds and assets through all points of the market cycle.

While income generation will not be unaffected, real assets yields are still likely to remain at a healthy spread to bonds. With the world continuing to pursue lower-for-longer interest rates, the relative attractiveness of real assets should remain a fixture beyond the current market turmoil.

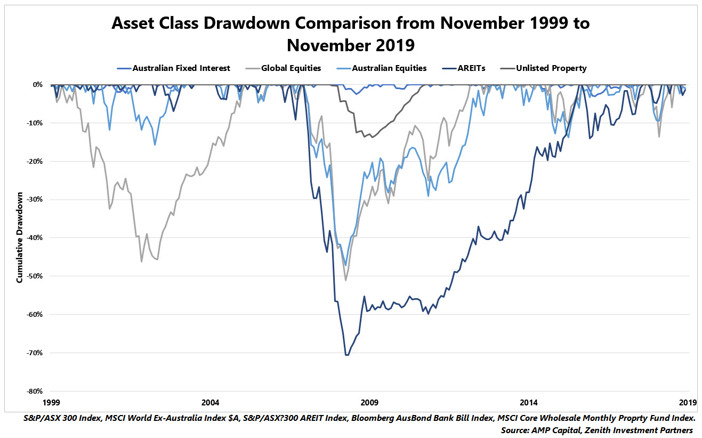

It also pays to remember that in a portfolio context, real assets tend to have a much lower drawdown profile than liquid investments. As an example, the following chart shows the asset class drawdowns across liquid securities and unlisted real estate funds. While it is too early to tell what the 2020 drawdown profile looks like, the characteristics of real asset fundamentals and unit pricing should result in a lower drawdown profile in the current environment.

We believe the sector continues to offer a strong proposition for those seeking to access physical assets which have many attractive characteristics in a portfolio context. Even in current conditions, a place remains for illiquid assets in clients’ portfolios.

However, the decision to maintain exposure to such assets must be highly sensitive to illiquidity risk tolerances. We believe that the full potential of these assets can only be realised in a strategy that is liquidity constrained. As such, it is vital to ensure that portfolios are appropriately constructed to deal with real asset allocations to ensure optimal outcomes.