Amidst the heightened volatility created by the COVID-19 outbreak, many investors are rightly asking the question “should I rebalance my portfolio? And if so, when is the right time?” There are various rebalancing methods that can be applied, based on frequency, rules or triggers.

It’s important for investors to understand the costs and benefits of various approaches to rebalancing. In this article, we seek to compare rebalancing methodologies that can be applied to manage an investor’s portfolio.

How to Assess Rebalancing Methods?

When comparing the optimal rebalancing methods, a common approach is to assess the historical performance of each, concluding that the outcome with the strongest performance over the period is the best approach. We believe such an assessment is limited and highly dependent on market performance during the period.

For example, if rebalancing approaches are assessed during a bull market, a ‘no rebalance’ approach will come out on top as growth assets are allowed to run. Conversely, if the period selected features a downturn and subsequent recovery, a more frequent rebalancing approach is likely to outperform. The approach is able to more frequently capture the market at lower cost bases during the downturn and results in outperformance during the subsequent recovery.

We believe that investors need to consider much more than historical performance to select an appropriate rebalancing approach. First and foremost, we advocate that rebalancing should be used to ensure the purity of an investor’s strategic asset allocation (SAA) and to reduce potential drift.

This is very important for advisers from a compliance and risk perspective alone where a client has usually completed a Fact Find questionnaire and Risk Profile questionnaire and has agreed (in writing) with their adviser as to what risk profile or portfolio type is appropriate for their circumstances and risk appetite. Allowing a portfolio to drift away from a client’s agreed risk profile is therefore a major compliance risk for advisers.

This is particularly important with regards to the SAA for defensive and growth asset weights. Material deviations of these weights from SAA may result in risk/return characteristics that contradict the investor’s long-term objectives. For example, a typical ‘balanced’ investor may have a defensive and growth SAA of 40% and 60%, respectively. If performance drift caused growth assets to rise to 65%, the investor’s portfolio may have a higher expected return potential than the SAA implies, but it would also subject the investor to an increased level of risk that they may not be capable or willing to accept.

Other important consideration when assessing rebalancing methods is the transaction costs and potential tax involved. A more frequent rebalancing approach will reduce drift of the portfolio from SAA but will also incur a greater level of transaction costs and potential tax costs (for those investors outside a superannuation or pension mode). Investors need to be mindful of this trade off when determining an appropriate approach.

Comparison of Rebalancing Methods

In the following analysis, we seek to compare the outcomes of the following four rebalancing approaches when applied to a ‘balanced’ portfolio (40% defensive assets and 60% growth assets):

- No rebalancing

- Annual rebalancing

- Quarterly rebalancing

- Subjective rebalancing

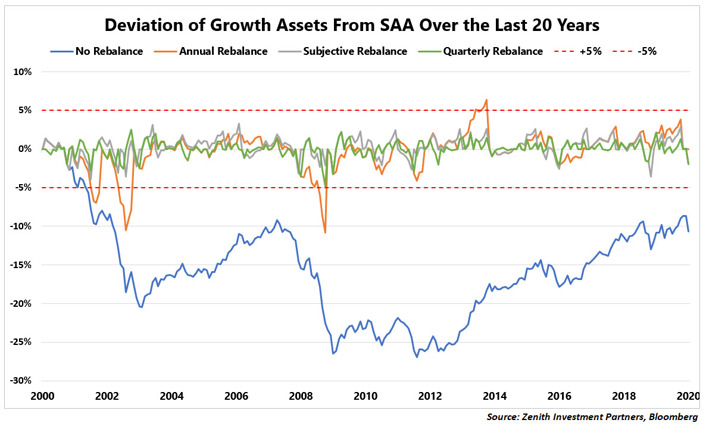

The chart below shows the deviation of growth asset weights from the growth assets SAA (60%) for the last 20 years. We have also plotted lines for +/-5% deviation from SAA as we believe this is an unacceptable drift and contradicts the investor’s risk profile.

In addition, we have measured each approach (excluding transaction fees and tax) by the metrics in the table detailed below:

| No Rebalance | Annual Rebalance | Quarterly Rebalance | Subjective Rebalance | |

|---|---|---|---|---|

| Average Deviation | -15.57% | -0.26% | 0.00% | 0.28% |

| Maximum Deviation (Absolute) | 26.92% | 10.84% | 4.78% | 3.98% |

| Number of Trades Required | 0 | 21 | 80 | 28 |

| Average Magnitude of Trades | 0.00% | 2.56% | 1.16% | 2.70% |

| Proportion of Periods Outside Deviation of +/-5% | 92.95% | 6.22% | 0.00% | 0.00% |

The no rebalance approach provides the worst outcomes out of the four methods. Due to the sharp drawdown in the early 2000s, the method results in a growth weight that is well below SAA and never recovers over the 20-year period. This is a sub-optimal outcome for investors as their ability to generate returns in line with their risk profile objectives is severely hindered as their growth asset allocation is persistently underweight. The only benefit of this approach is that no trades are required and therefore transaction costs are kept to a minimum.

The annual rebalance approach improves upon the no rebalance approach as the average deviation is much closer to zero. As expected, this approach requires more trading as a rebalance is conducted each year which ultimately increases transaction costs. However, the approach still falls outside the acceptable +/-5% range in 6.22% of all periods. This is a result of sharp drawdowns that occur in less than one year.

In terms of the appropriate drift, the quarterly rebalance approach further improves the outcome as it has an average deviation of 0.00% and has no periods where drift is outside the +/-5% range. However, this tight tracking comes at the cost of significantly increased trading and potential tax costs as a rebalance is required every quarter. This will vastly increase the transaction costs such as brokerage and buy/sell spreads but will also create more frequent crystallisations of tax which ultimately increase taxable gains for the investor. The steep rise in these costs outweighs the tight tracking around SAA weights.

The subjective rebalance approach is a happy middle between all these outcomes. As the method will only trigger a rebalance where drift is outside the range of +/-2%. This ensures that there are no periods in which drift is outside the +/-5% range while keeping the number of transactions to a minimum, especially when compared with the quarterly rebalance approach.

How do we rebalance our portfolios?

As reinforced by the comparison above, we believe that a subjective rebalance is the most prudent approach to ensure that neither defensive/growth drift nor transaction costs are excessive, and the integrity of a client’s agreed risk profile is maintained and not breached. The subjective rebalance will only trigger a rebalance when required as per the defensive growth/drift rather than periodically.

While the subjective rebalance is still a rules-based approach, it allows for qualitative overlay which can be beneficial in extraordinary circumstances. In the current environment, volatility is far above normal conditions due to the COVID-19 outbreak. Over the last month, we have seen drastic market moves in both positive and negative directions. These large moves may potentially counteract any rebalancing action or cause an overshoot.

In these circumstances, the subjective rebalance allows for a qualitative decision to be made that may result in a partial rebalance or even no rebalance action if substantially justified. Additionally, in times of significant market downturn, buy/sell spreads may widen due to low liquidity in markets (which has already occurred in fixed interest-based products / ETFs). Again, the subjective rebalance can take the widening of spreads into account unlike a systematic approach to rebalancing.

Conclusion

While it is natural to compare past performance of rebalancing methods, we urge investors to dig deeper in their analysis and prioritise the defensive/growth weights drifts to ensure the purity of portfolio SAA and clients’ agreed risk profiles. We assert that a subjective rebalance provides an optimal balance between defensive/growth drift and transaction costs and qualitative overlay can provide additional benefit during times of market stress.

Important notes

The benchmark used for the rebalance analysis comprises the following:

- 30% MSCI World ex Australia (AUD Hedged)

- 30% MSCI World $A Unhedged

- 40% Bloomberg Barclays Global Aggregate Index (AUD Hedged)

The following rebalance rules are applied:

- No rebalance – the portfolio is never rebalanced

- Annual rebalance – the portfolio is rebalanced at the end of each calendar year

- Quarterly rebalance – the portfolio is rebalanced at the end of each quarter (end of March, June, September and December)

- Subjective rebalance – the portfolio is rebalanced if the defensive/growth drift exceeds +/-2% at the end of each month

By James Damicoucas, Investment Consultant