By Calvin Richardson, Investment Consultant

Financial markets entered 2022 nervously, with central bankers walking a tightrope to tame inflation whilst aiming to execute a soft-economic landing. The subsequent correlated sell-off in equity and bond markets has left investors with few places to shelter from the market’s tumult, with fears that the fever-dream for markets might finally be over.

The Russian invasion of Ukraine has further compounded these anxieties, as countries were forced to reroute their energy supply chains to counter Russian aggression. However, with Russia supplying 11% and 17% of global oil and gas supplies respectively, this has material implications for energy inflation.

Russian for the exit

Commodity price shocks, central bankers nervously tightening into a slowdown, and China steadfastly committed to widespread lockdowns has understandably led to skittish market sentiment.

These mounting economic and geopolitical crosscurrents have markets in disarray, with our portfolio performance not immune to these headwinds. Fortunately, we have intentionally constructed our portfolios to provide downside protection during risk-off scenarios, with multiple levers providing uncorrelated and differentiated return drivers.

We have long cautioned of the asymmetric risk associated with rising rates and therefore structured our portfolios to exhibit materially lower interest rate duration than the benchmark. Over the quarter, this positioning performed as expected and delivered our investors attractive relative outperformance versus the blowout experienced in long-duration bond exposures.

Whilst still maintaining a core allocation to benchmark aware duration anchors, our investments in managers targeting capital preservation through a defensive low-duration stance paid-off through the Ardea Real Outcome Fund, Pendal Dynamic Income Fund, and the Janus Henderson Tactical Income Fund.

Another bright spot has been our Alternatives line-up, which has successfully dampened volatility whilst delivering positive absolute returns amongst the broader market ructions. This was largely attributable to our managed futures allocations where the Aspect Diversified Futures Fund and the Man AHL Alpha Fund expressed directional views capturing trend signals across equities and bonds, and non-mainstream assets, such as gold, commodities, currencies, and options. Likewise, performing as expected was the Janus Henderson Global Multi-Strategy Fund which mitigated the market’s left-tail risk through an options protection overlay which delivers positive returns when equities fall.

May mayhem

Unfortunately, detractors elsewhere in the portfolio overrode these contributors, which has seen our capital preservation fall short of expectations over the short-term. We can isolate the cause of this underperformance to a couple of overarching biases, which we believe remain a valid part of our portfolio construction.

Firstly, in efforts to neutralise our domestic benchmark’s large weighting to energy, several of our managers with a ‘quality’ emphasis in their security selection were materially underweight the energy sector. Examples include the L1 Capital International Fund, Magellan Global Fund, Fairlight Global Small & Mid Cap (SMID) Fund, Lennox Australian Microcap Fund, and the Bennelong Ex-20 Fund.

Between a rock and a hard place

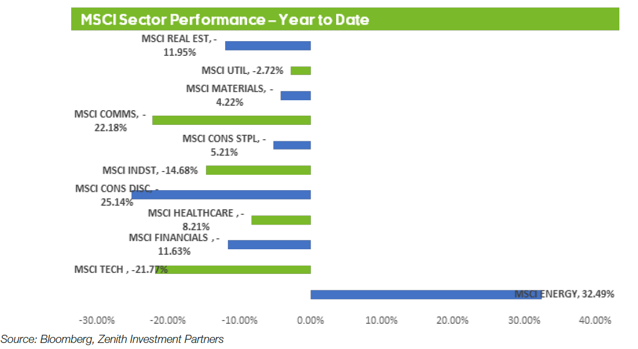

As the chart below highlights, market conditions have been extraordinary, with the energy sector providing the sole source of positive returns for the MSCI World. Consequently, this positioning hurt relative returns where managers were underweight or naked.

Given these managers prioritise ‘quality’ characteristics such as low leverage and predictable earnings growth, they’ve instead opted to access this cyclicality through second derivative avenues. For example, L1 gains exposure to the economic cycle through building materials, whilst Bennelong are leveraging food inflation through the agriculture space.

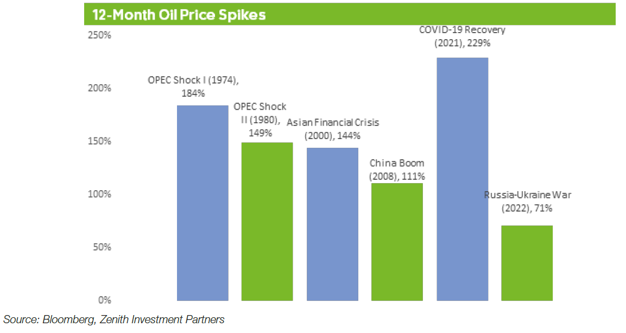

Although our underweight positioning has detracted from performance in the short-term, our aggregate portfolio exposure has been neutral energy. It’s also important to highlight that these outsized moves in oil have few historical precedents, with only five instances where oil has doubled over 12-months since the 1960’s.

To contextualise these price spikes, this quantum of outperformance has only been observed in 3% of rolling 12-month periods over this horizon. As such, managers are approaching the sector cautiously as these gains are susceptible to a disorderly unwinding due to the war premium incorporated into the oil price.

Substance over style

Another crucial headwind over the quarter has been our intentional bias to the ‘quality’ style-factor within our International Shares sleeve. This is due to the defensive characteristics associated with ‘quality’ companies (e.g., high barriers to entry, low leverage, high profitability) which are better equipped to withstand periods of economic weakness.

The trade-off associated with these protective elements is that ‘quality’ oriented companies can trade on higher multiples which can quickly de-rate when bond yields unexpectedly jag higher. Similarly, during this period of underperformance, the market hasn’t been focussed on earnings, and our underlying companies have been punished irrespective of their business strength, competitive industry positions and strong financials.

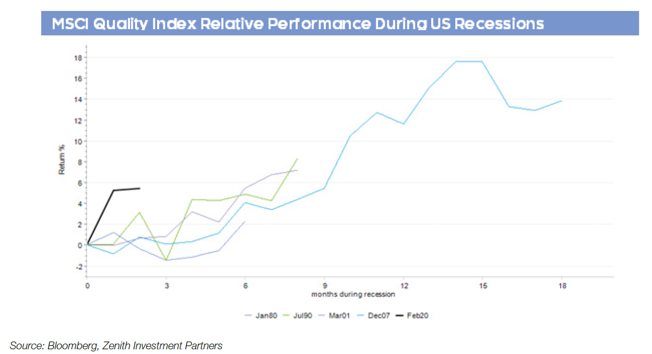

Importantly, once normal market dynamics are restored, these companies which have been indiscriminately sold, offer the potential for strong upside. This is supported by our research which shows that the ‘quality’ factor in International Shares has generated over 3% outperformance p.a. dating back to the 1980s, so we remain comfortable with this modest tilt.

Health check

Nevertheless, this style of investing is not resistant to short-term gyrations in share prices and can, at times, exhibit performance which meaningfully deviates from the benchmark.

Despite ‘quality’ companies being swept up in the market’s indiscriminate selling, we remain confident that the market will reprice the fundamentals as the extreme risk aversion subsides. In fact, our managers are taking advantage of the dislocated markets and adding to their positions in multiple high-quality businesses trading at attractive prices.

As always during bouts of volatility, we remain in constant contact with our underperforming managers and retain confidence in their ability to navigate these uncertain times. And although we remain susceptible to short-term volatility, we retain confidence in these highly experienced managers and believe their defensive characteristics will reassert themselves over the medium-term.

Whilst markets teach and the lessons can be painful, remember that recoveries from corrections begin when sentiment is excessively bleak, and making hasty portfolio decisions could be to the detriment of your long-term objectives.