Market participants, especially equity investors, can be forgiven if the words déjà vu spring to mind during this COVID-19 period. Although there are definite similarities between the Australian equity market drawdowns and subsequent recoveries of COVID-19 and the global financial crisis (GFC), COVID-19 has proven to be the GFC in fast-forward. That is, during this period, we have seen the fastest bear market in Australian equity history.

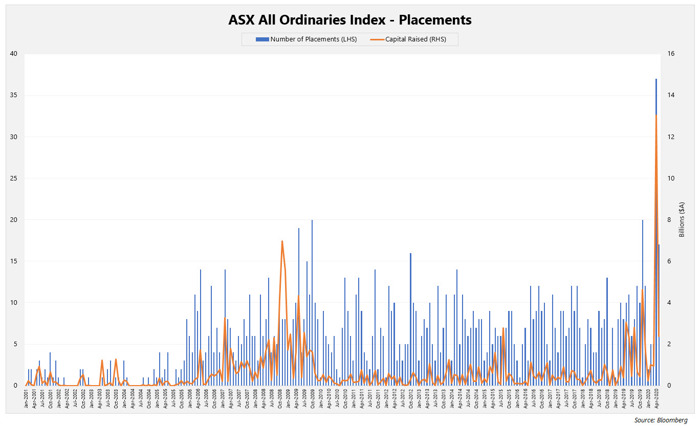

As experienced in the GFC, the deterioration of the economy resulted in companies raising capital to shore up balance sheets. However, unlike the GFC, we have found that this time around, companies with growth ambitions also took the opportunity to tap the market for additional capital. As a result, April 2020 was a record-breaking month, with 37 placements raising a total of $A 13 billion.

Although capital raisings can take many forms, our analysis focuses on placements. A placement occurs when a publicly-traded company issues new shares to raise capital. New shares are offered to a select group of investors, typically institutional investors.

The purpose of a placement is to be a funding source, used for a variety of reasons, including ambitions to grow operations, develop new products and/or services, or even to fund operations during loss-making periods. During COVID-19, we have observed a sharp spike in the number and size of capital raisings from placements.

To see a similar spike in the number and size of capital raisings from placements within a single month, we need to look back to the global financial crisis (GFC) period. In October 2009, the number of placements topped 20 and in November 2008 total funds raised hit a month high of $A 7 billion.

What is different this time?

On 1 April 2020, the Australian Stock Exchange eased capital raising rules, which permitted companies to raise additional capital due to COVID-19. Up until 31 July 2020, companies can raise up to 25% of their capital on issue without shareholder approval, as opposed to the usual limit of 15%. With this temporary rule change, companies such as Flight Centre and NAB were able to shore up balance sheets at a rate reminiscent of the GFC.

Conversely, we have observed company behaviour that was somewhat opportunistic, with companies that were unimpacted or less impacted by COVID-19 also raising capital. Rather than fortifying their balance sheets, companies such as NextDC and Breville raised capital for growth initiatives such as acquisitions and investment.

How have the placements performed?

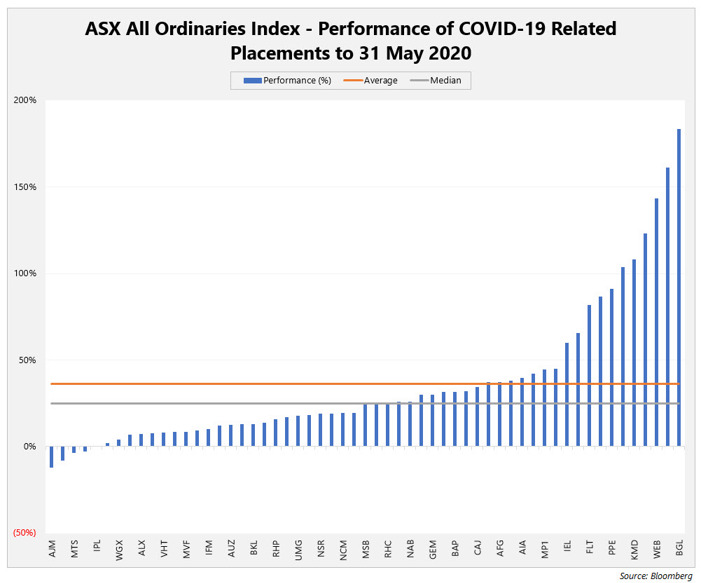

To assess performance, we have analysed the offer price of each placement announced post 21 February 2020, comparing the offer to the company’s share price as at 31 May 2020.

As the chart highlights, participation in placements in this period has been generally rewarding for investors.

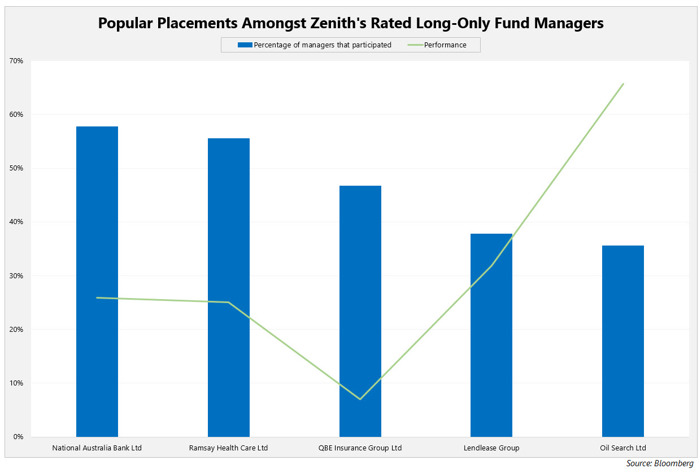

Which placements were popular amongst Zenith’s rated long-only fund managers?

Of the 57 placements during this period, our managers participated in 43. The most popular placements amongst our rated long-only fund managers and the performance from their respective announcement dates to 31 May 2020 are shown in the chart below.

As expected, the highest participation rates were in the larger, more liquid stocks, with the five most popular capital raisings all members of the S&P/ASX 50 Index.

Which investment style benefitted from the placements?

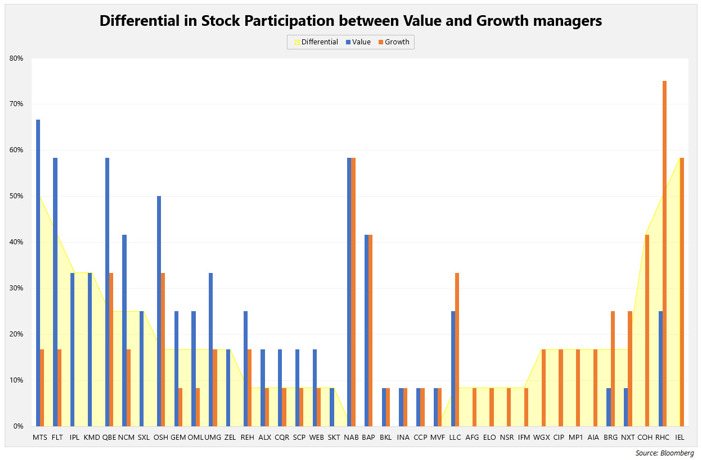

During the GFC, value managers were the key beneficiaries of the raft of placements that were brought to market. However, we did not observe a clear trend that demonstrated greater participation by value managers compared to growth managers during the COVID-19 period.

We found that value funds participated in 38% of all placements, whilst growth funds participated in 32%. We believe there has been a higher than expected participation rate from growth funds in placements compared to their participation during the GFC. This was a result of the heightened number of opportunistic placements that occurred for acquisition and growth purposes, which were not apparent during the GFC.

Unsurprisingly, value managers were prominent in the placements of more distressed companies such as Metcash, Kathmandu and Flight Centre. Whilst companies without balance sheet issues such as Ramsay Health Care, IDP Education and Cochlear were popular amongst the growth managers.