For disciplined investors, the market volatility observed throughout 2020 provided fertile hunting ground for investment opportunities at bargain basement prices. As typically occurs during market selloffs, markets overreact, which exposes mispriced opportunities for experienced investors to capitalise on.

Pleasingly, our risk-aware portfolio construction and concerted emphasis on drawdown minimisation meant our portfolios experienced a softer pullback compared to our diversified benchmark and many peers. Likewise, our adherence to a strict rebalancing regime over this period meant investors benefited from our rotation into equity markets trading at depressed prices.

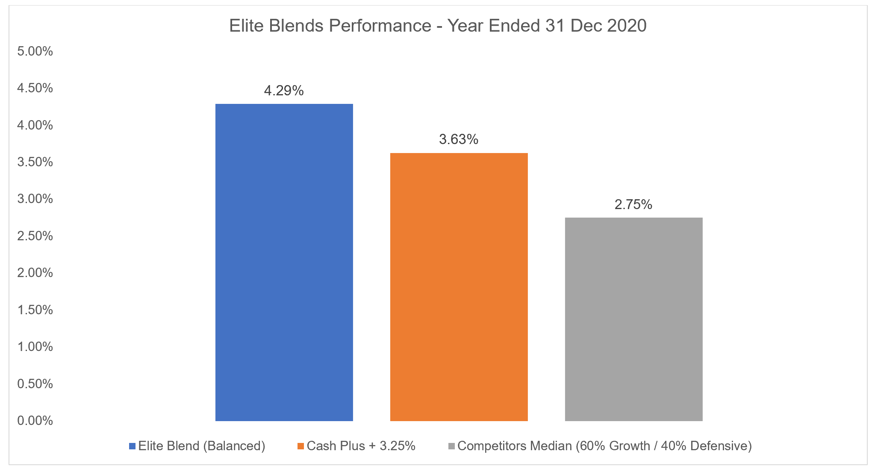

Source: Zenith

Diversified return drivers provide support

Due to the diversified nature of our portfolios, there were various levers available which cushioned the impact of the initial market pullback. Whilst equity markets struggled, some of our managers with ‘shorting’ capabilities proved resilient and were able to generate modest profits to offset broader market losses. Equally, our suite of alternatives provided an uncorrelated and differentiated return stream to buffer the market volatility and enhance returns.

Most notably, the market neutral allocation exceeded expectations with admirable defensive characteristics demonstrated during the initial market turmoil, only to also generate healthy returns when the market rallied. Furthermore, the global macro and managed futures exposures buoyed overall portfolio performance through cushioning the drawdown whilst still delivering modest performance in the reversal.

We have long recognised the importance of alternatives in portfolio construction due to the downside protection exhibited during market weakness. And whilst the speed of the market correction was unprecedented, the performance of our preferred alternatives managers was not, as these allocations performed in-line with expectations and provided offsetting gains against the broader market turbulence.

Don’t worry, fixed income is still relevant

Importantly, whilst the ‘traditional’ fixed income portion of the portfolio demonstrated defensive characteristics during the early bouts of market volatility, these segments also delivered attractive returns for the remainder of the year. As investors flocked to the safety of government bonds and high-grade corporate debt, this resulted in material price appreciation of the fixed income securities held in our portfolios. However, during this period it was crucial to avoid bonds which carried any solvency concerns, and again, illustrated the importance of active management to navigate this unchartered terrain.

To ignite economic growth, interest rates were slashed to rock-bottom which provided a short-term sugar hit to our ‘traditional’ fixed income managers. However, this now challenges the ability for yield-starved investors to generate meaningful income and emphasises the importance of allocating to ‘unconstrained fixed income’ managers. These managers can flexibly manoeuvre their portfolios by shifting allocations across undervalued fixed income sectors to generate incremental outperformance. This allows managers to take advantage of higher yielding opportunities without compromising on risk-control.

2020 not your average year

The unprecedented stimulus offered through governments and central banks meant that 2020 was far from a ‘typical’ recession. From April to the end of the year, markets seemingly enjoyed an upward trajectory and managed to shrug off subsequent lockdowns, political pressures and international stoushes.

This renewed optimism in the latter half of the year spurred material gains across our portfolios, particularly within the Australian shares sleeve which has historically delivered strong outperformance. Admittedly, this segment did struggle early in the year when markets were skittish, however, as risk-on sentiment came flooding back, these exposures roared to life and generated strong outperformance.

Unfortunately, our listed property and infrastructure exposures were not immune to the disproportionate drawdowns observed in these sectors, as global lockdowns crimped previously healthy markets. Nonetheless, these asset classes continue to offer attractive yield and diversification advantages, which provides comfort in our long-term Strategic Asset Allocation (SAA) construct.

All portfolio inputs play a vital role

The ‘quality’ bias inherent within the international shares portion of the portfolio largely drove the capital preservation when markets were choppy. This mild skew towards the ‘quality’ factor is intentional as we believe that companies exhibiting ‘quality’ characteristics (e.g., high barriers to entry, strong balance sheets, etc) are better equipped to withstand periods of market distress.

This complements the modest ‘growth’ tilt observed in the Australian shares segment, which as noted has strongly aided returns in rising markets. From a holistic portfolio perspective, the core focus is on blending complementary investment styles, which in isolation are not expected to outperform at every stage of the investment cycle; however, in aggregate, will demonstrate long-term outperformance whilst not taking any unintended sector or factor bets.

The resulting portfolio is predominantly style neutral to ensure that diversified return drivers enable attractive, risk-adjusted returns irrespective of market conditions. Importantly, we don’t construct portfolios based on short-term forecasts or trending themes, and instead, look to build ‘all-weather’ portfolios. Notably, this served our investors well, as our Consulting team took a disciplined approach when markets were wavering and applied our long-term investing approach to see through the noise.

Stay the course

Whilst the heightened volatility throughout the year may have been unnerving for many, it demonstrated the value in actively managed portfolios, whereby short-term market dislocations could be exploited by professional investors. The tumultuous nature of 2020 likewise underscored the importance of active management to minimise losses and rebalancing to capture the totally unexpected upswing in markets which defied many naysayers.

There’s no doubt that investment markets, and the economy more broadly, delivered some unexpected events for portfolio managers; however, our portfolio construction methodology, monitoring and rebalancing processes enabled us to deliver strong performance for the year. Encouragingly, our FUM grew to over $2bn of client assets and we also assisted an increasing number of professional advice businesses across the country to deliver truly client-focussed outcomes.