Australian bank hybrids have long been a favourite in income-focused client portfolios for their combination of regular income, tax benefits through franking credits, and the reassurance of major bank backing making them easy to recommend and easy for clients to understand. But all of this is now changing. The Australian Prudential Regulation Authority (APRA) has confirmed that hybrid securities will be phased out of the Australian market, beginning in 2027 and for advisers, this raises a straightforward question: what do we use instead?

The short answer is that there are suitable, robust options available and the market has already moved to fill the gap. And clients with hybrid exposure don’t need to sacrifice income to make the transition.

Why are hybrids being phased out?

Hybrids were designed to act as a financial safety net, so if a bank ran into serious trouble, these securities could absorb losses and protect depositors, converting them into shares or being written off before the bank itself failed.

The problem is they never really worked that way, so when Credit Suisse collapsed in 2023, hybrid investors lost their money at the point of failure, not before. APRA looked at that outcome and concluded that Australian hybrids had the same flaw: in a real crisis, they wouldn’t provide the protection they were designed to.

Rather than tinker with the structure, APRA decided to remove hybrids from bank capital entirely and replace them with simpler instruments that behave more predictably. The overall amount of capital banks hold stays the same; the change is about making each part of that capital do what it’s supposed to do.

What your clients valued in hybrids

Before thinking about alternatives, it’s worth being clear about what made hybrids attractive in the first place and four things stand out:

- regular income: hybrids paid distributions that moved with interest rates, which suited clients seeking predictable cash flow

- franking credits: fully franked distributions delivered a meaningful tax benefit, especially for retirees and lower-tax investors

- familiar issuers: being issued by the major banks gave clients a degree of comfort about the underlying credit quality, and

- strong returns: over the long term, hybrids delivered solid income returns relative to the level of risk most clients perceived they were taking.

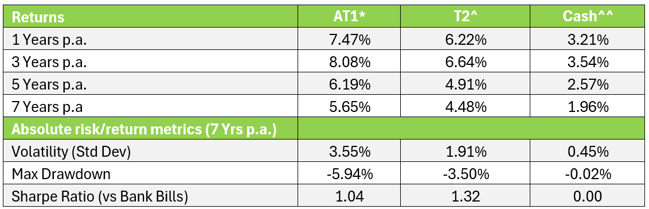

*AT1: Solactive Australian Banking Preferred Shares GTR Index, ^T2: Solactive Australian Major Bank Subordinated FRN Index, ^^Cash: Bloomberg AusBond Bank Bill Index. Data as at 22 June 2026.

What happens, and when?

The phase-out doesn’t happen overnight, so existing hybrids will be retired gradually from 2027 through to 2032 as each security reaches its scheduled maturity date. Each of the major banks has its own dedicated timeline to manage this process too.

The hybrid market has already started to shrink. Over the past two years, it’s contracted from around $43 billion to $34 billion, and with no new hybrids being issued, that trend will continue. As the pool of available securities gets smaller, pricing has tightened and liquidity has reduced. Fund managers have been responding by gradually moving client money out of hybrids and into alternative fixed income strategies, so most of that rotation is already well underway.

Why the transition is more straightforward than it sounds

Two things have made this transition easier than many expected.

First, the banks themselves have been busy issuing replacement securities. To meet new regulatory requirements, the major banks significantly increased their issuance of subordinated bonds which are a simpler type of fixed income security that sits just below hybrids in the capital structure. That supply has given fund managers a ready-made place to put money to work.

Second, international banks have also been active in the Australian market, bringing additional variety and helping to keep the supply of quality fixed income securities healthy. The result is that the Australian credit market is in good shape to absorb the hybrid exit without a meaningful impact on income opportunities for investors.

What alternatives are available for your clients?

Beyond simply swapping hybrids for bank bonds, fund managers have developed a range of new strategies that aim to deliver comparable income. For example, franking credits won’t be replicated, which is worth noting as the most significant change for tax-sensitive clients, but the income itself can be maintained. Beyond that, there are three alternative types of strategy worth understanding.

Listed notes

These are ASX-listed securities that work similarly to hybrids in terms of how clients experience them, i.e. regular income distributions, listed on the exchange, and a fixed end-date. The key difference is that the structure is simpler and the risk is more transparent. Some include a buffer where the manager absorbs any losses up to a certain level before investors are affected. These are a natural first conversation for clients who currently hold hybrids and want something familiar.

Credit-focused ETFs

These are exchange-traded funds that invest across a range of Australian fixed income securities, and are actively managed to generate income above the cash rate. They offer daily liquidity, are straightforward for clients to understand, and are well suited for clients who valued hybrids for their income but don’t need the listed familiarity.

Leveraged investment grade credit

This option is a more sophisticated approach, where managers use borrowing to amplify the income from high-quality bond portfolios. The credit risk remains investment grade and, in many cases, stronger than the underlying credit risk of hybrids, but the income generated can be comparable. These strategies are best suited to clients who understand that leverage is involved and are comfortable with how that can affect returns.

What this means for you and your clients

The phase-out of hybrids is one of the bigger changes to hit the Australian fixed income market in recent years, but for advisers, the practical implications are manageable.

The income your clients relied on from hybrids can be maintained through alternative strategies and with the transition happening gradually, it gives you time to review portfolios thoughtfully rather than reactively. In addition, the product landscape has genuinely improved as there are more options available today than there were two years ago.

The main changes to work through with clients are the loss of franking credits for those who valued them, and ensuring replacement strategies match each client’s income needs, time horizon, and comfort with complexity.

Zenith’s investment research team is actively monitoring this space and assessing new strategies as they come to market, supporting advisers in understanding complex products suitable for the retail market. If you’d like more information about our investment research capability, contact Doug Hope.